Definition of Equity in Accounting: How Does it Work?

Equity in accounting is a critical measure of a company's financial health. A key component on any balance sheet, it offers insights into a company's net worth and guides investors and financial analysts in assessing the value and performance of a business.

What is Equity in Accounting?

Equity in accounting is the value left in a company after accounting for all its assets and subtracting its liabilities. This figure, often referred to as "shareholders' equity" or "owner's equity," is a fundamental indicator of a company's financial health and performance. It's showcased on a company's balance sheet and comprises various elements, including retained earnings, common stock, and additional paid-in capital.

In simpler terms, equity represents an ownership interest in the company. For instance, if a company owns assets like buildings and technology (tangible assets) and patents (intangible assets), these contribute to the company's total assets. From this total, if you subtract all liabilities, like loans or debts the company owes, what remains is equity. This concept also translates to personal equity, where an individual's personal assets minus their personal liabilities equal their net worth.

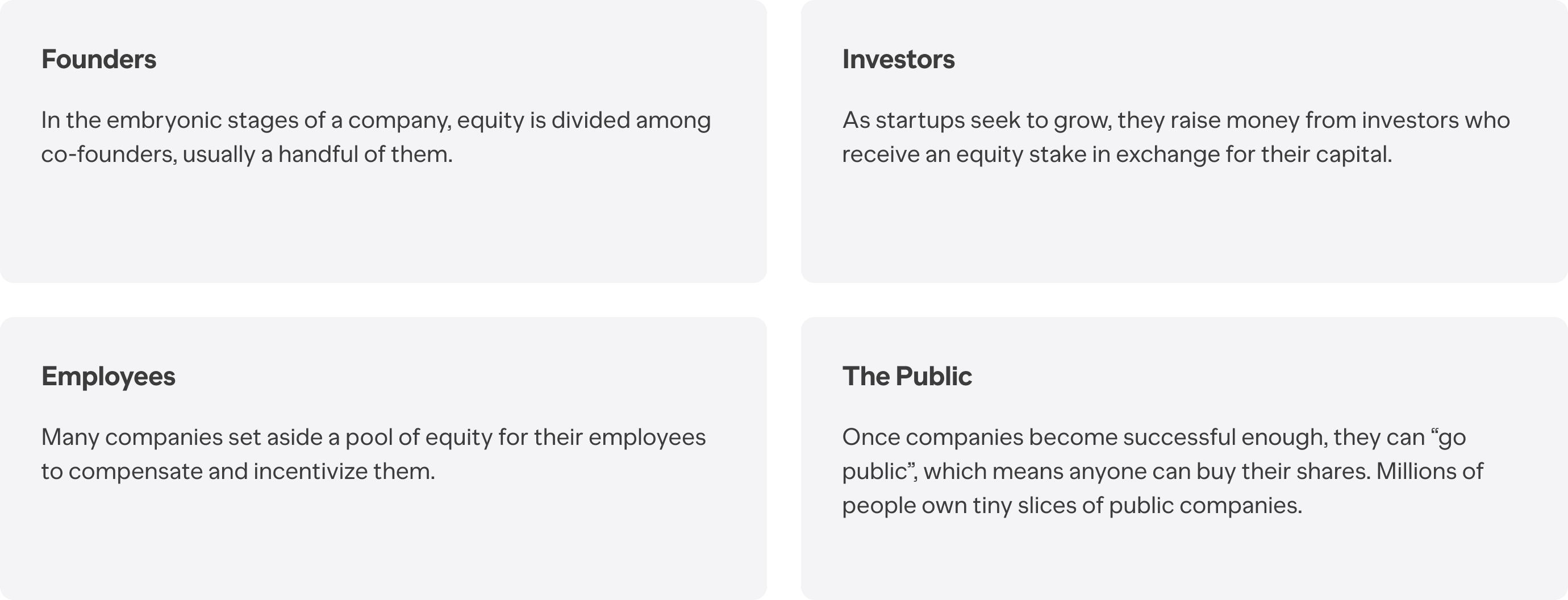

To calculate equity, accounting statements use a straightforward formula: Total Assets minus Total Liabilities equals Equity. This basic calculation can reveal a lot about a company, including its ability to cover debts and fund its operations, making it a crucial point of analysis for investors, financial analysts, and accounting firms. There are four broad categories of equity owners:

Why is Equity Important for Businesses?

Equity is a crucial element for any business, large or small. It's more than just a number on a balance sheet; it's a reflection of a company's net worth and financial strength. Equity is important for several key reasons:

- Indicator of Financial Health: Equity offers a snapshot of a company’s financial health. A positive equity value, where a company's assets exceed its liabilities, suggests a strong financial position. Conversely, negative equity can be a red flag, indicating potential financial troubles.

- Attracting Investors: Investors often look at a company's equity to gauge its financial performance and growth potential. Higher equity value can attract more investors, as it implies the company has more assets than liabilities, making it a potentially safer investment.

- Basis for Equity Financing: When a company needs capital, it can turn to equity financing – selling shares of stock to raise funds. This is where equity’s role becomes critical. Investors are more likely to invest in a company with strong equity, as it often means the business is stable and has growth potential.

- Impact on Market Value: While book value of equity is calculated from the balance sheet, the market value of equity is what investors are willing to pay for it. A strong equity position can positively influence a company’s market value, enhancing its reputation and standing in the business world.

- Influence on Additional Financial Decisions: Equity isn't just about the value of shares or total assets; it also influences other financial decisions and strategies. For instance, a company with solid equity might be in a better position to take on debt for expansion, knowing that its assets provide a safety net.

Equity on a Balance Sheet Explained

Equity is a key section on a company's balance sheet, sitting alongside assets and liabilities. Understanding how it fits into this financial statement is crucial for anyone looking into a company’s financial health.

- Position on the Balance Sheet: Equity is typically found at the bottom of the balance sheet. It's calculated after listing out all assets and liabilities. The basic formula here is: Total Assets minus Total Liabilities equals Equity.

- Components of Equity: Equity on a balance sheet is not just a single number. It comprises several elements, including retained earnings, common stock, and additional paid-in capital. Retained earnings are the profits a company has kept over the years, not distributed as dividends. Common stock and additional paid-in capital reflect the initial and additional funds brought in by shareholders.

- Reflection of Company Value: The equity value is a direct reflection of a company’s net worth. This is the value that theoretically would be returned to shareholders if all assets were liquidated and all debts paid off.

- Variation by Company Type: Equity can vary significantly depending on the type of company. For instance, in publicly traded companies, equity includes shares outstanding, which represents the total number of shares owned by stockholders. In contrast, a privately-owned business might have a simpler equity structure, primarily composed of owner's equity and retained earnings.

- Negative Equity: Sometimes, a company might have negative equity. This situation occurs when liabilities exceed assets. Negative equity is a warning sign, often indicating financial distress.

- Equity and Financial Analysis: For financial analysts and investors, equity is a crucial part of assessing a company’s financial performance. It helps in understanding how well a company is managing its assets and liabilities over time.

Book Value vs Market Value of Equity

Understanding the difference between book value and market value of equity is crucial for anyone involved in business, investment, or accounting.

- Book Value of Equity: The book value of equity is derived directly from a company's financial statements, specifically the balance sheet. It's calculated by subtracting total liabilities from total assets. This value is often considered the net worth of the company from an accounting standpoint. It includes tangible assets like buildings and machinery, as well as intangible assets like patents and trademarks. However, it's important to note that book value is based on the cost of assets, not their current market value.

- Market Value of Equity: In contrast, the market value of equity reflects what investors are willing to pay for the company's stock in the open market. This value can be calculated by multiplying the current stock price by the total number of outstanding shares. Market value is influenced by factors like the company's future profit potential, investor sentiment, and overall market conditions. It’s a dynamic value, changing with market perceptions and conditions.

- The Gap Between the Two Values: Often, there's a significant gap between book value and market value. For instance, if investors believe a company has strong growth potential, its market value may far exceed its book value. Conversely, if the market lacks confidence in a company, its market value may fall below the book value.

- Implications for Business Decisions: The difference between these two values is critical for business owners, investors, and financial analysts. Book value provides a baseline, but market value offers a more current and dynamic perspective. Investment decisions and assessments of a company’s financial health often rely on understanding both these values.

Stock vs Equity in Accounting

In the realm of accounting and finance, the terms 'stock' and 'equity' are often used interchangeably, but they have distinct meanings.

- What is Stock?: In accounting, stock refers specifically to the share capital of a company, representing the ownership stake. It's divided into shares, each of which constitutes a unit of ownership. There are different types of stock, like common stock and preferred stock. Common stock typically gives shareholders voting rights and a share in the company's profits through dividends. Preferred stock, on the other hand, usually doesn't provide voting rights but offers a higher claim on assets and earnings.

- What is Equity?: Equity, broader in scope, represents the total value of a company's ownership interest. It's not just limited to stock but includes other elements like retained earnings (profits that are reinvested in the business rather than distributed to shareholders), additional paid-in capital (extra money paid by investors above the par value of the stock), and treasury stock (shares that the company has bought back).

- On the Balance Sheet: On a company's balance sheet, stock is a part of equity. Equity is the section that shows the value of all ownership interests in the company and is calculated as the company's assets minus its liabilities. Stock is one of the components that contribute to this overall equity value.

- Implications for Investors and Businesses: For investors, understanding the difference is crucial for investment decisions. Stock represents a more direct and specific investment in a company, while equity provides a broader view of a company’s financial health. For businesses, managing both stock and overall equity is key to financial stability and attracting investment.